Intense, real-world, memorable - gamified simulation training

Intense, real-world, memorable - gamified simulation training

In this Quantitative Trading Simulation, participants design algorithmic strategies, build predictive models, manage live execution, and optimize portfolios based on statistical signals in highly dynamic financial markets.

Algorithmic Strategy Development

Alpha Signal Research and Factor Modeling

Backtesting and Strategy Optimization

Market Microstructure and Execution Algorithms

Portfolio Construction for Quantitative Strategies

Real-Time Risk Management

Model Validation and Decay Monitoring

High-Frequency and Latency Considerations

Data Sourcing, Cleaning, and Alternative Data Integration

Performance Attribution and Analysis

In the simulation, participants will:

Analyze financial datasets to identify potential predictive signals.

Develop, code, and rigorously backtest trading algorithms.

Allocate capital and manage a multi-strategy quantitative portfolio.

Monitor live "market" feeds, manage order execution, and adjust strategies in response to real-time events.

Diagnose underperformance, distinguishing between bad luck, model decay, and broken assumptions.

Present strategy performance and research findings to a simulated investment committee.

Understand the end-to-end workflow of a quantitative trading operation.

Apply a systematic process for researching, testing, and implementing algorithmic strategies.

Evaluate trade-offs between strategy returns, risk, capacity, and turnover.

Recognize common pitfalls in quantitative finance, such as overfitting and look-ahead bias.

Interpret real-time market data and manage automated execution.

Communicate quantitative concepts and performance results effectively to stakeholders.

Develop judgment for when to trust a model versus when to intervene.

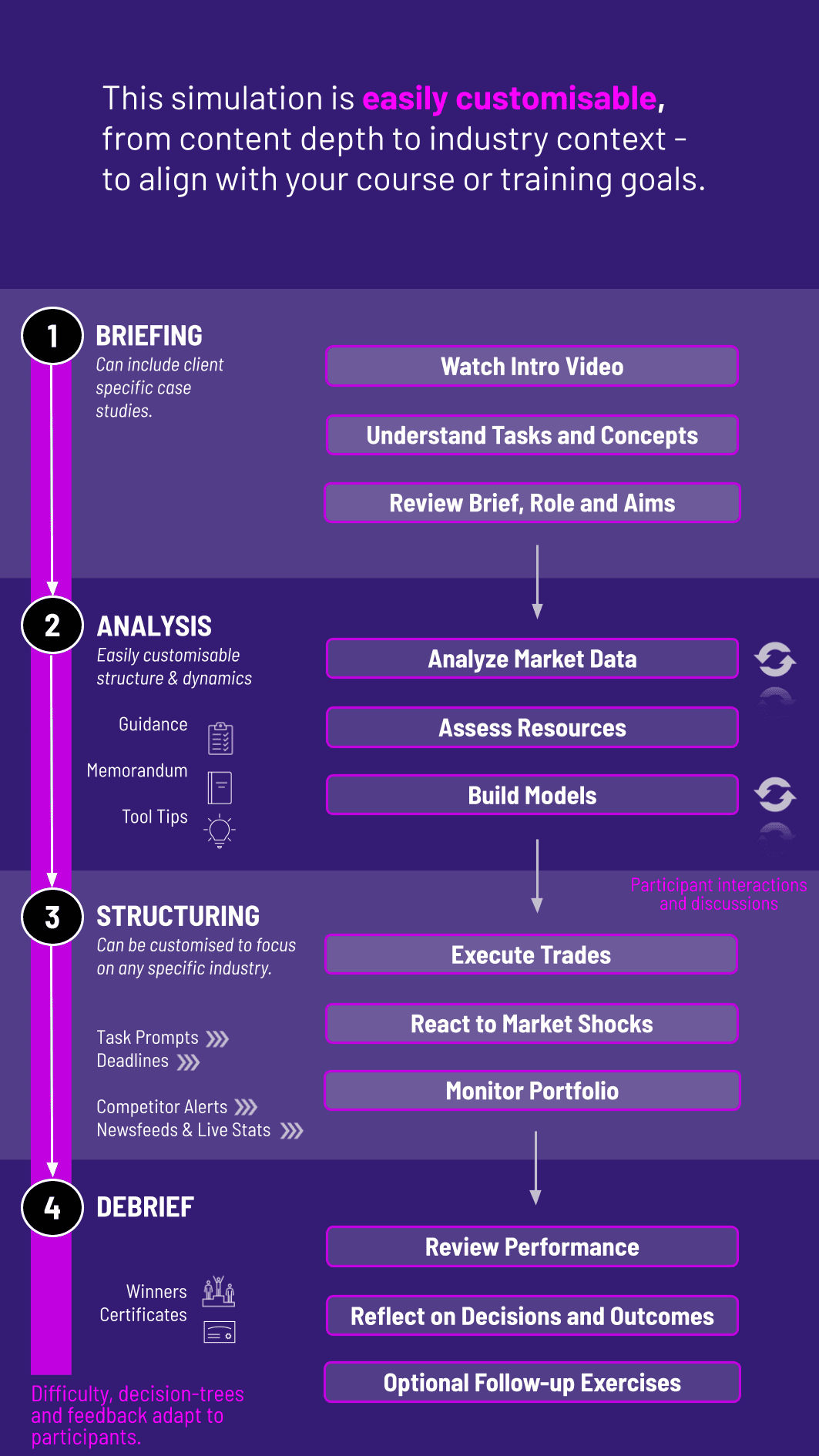

1. Receive Market Brief and Data Participants access a historical and real-time simulated market data feed across multiple asset classes.

** 2. Research and Development** They explore data, hypothesize signals, and develop trading logic using the simulation's tools.

3. Backtesting and Validation Participants run their strategies through historical scenarios, analyzing performance metrics and robustness.

4. Live Trading Rounds Approved strategies go "live" in a simulated market that reacts to participant orders and randomized news shocks.

5. Monitor and Iterate Teams monitor live P&L, risk metrics, and execution quality, making adjustments between rounds.

6. Review and Present The session concludes with a performance review, attribution analysis, and strategy presentations.

Who is this quantitative trading simulation designed for? It's designed for students and professionals pursuing careers in quantitative finance, algorithmic trading, data science in finance, and hedge funds.

Do I need prior programming or advanced math experience? While helpful, it's not required. The simulation provides structured environments for strategy logic and focuses on conceptual understanding; advanced coding can be incorporated for customizability.

How long does the simulation run? A standard session runs 4-6 hours, but it can be segmented into modules (e.g., research day, trading day) or extended for deep-dive workshops.

Is this simulation individual or team-based? It is optimized for team-based play, mimicking the collaborative nature of a quant trading desk, but supports individual participation.

What programming or tools are used? The simulation is a self-contained platform. Strategy logic is often built using formula-based or block-based interfaces, with options for Python/R snippets in advanced modes.

Is the market data realistic? Yes, the simulated data is designed with realistic statistical properties, volatility clusters, and correlations based on historical market behavior.

Can the simulation focus on specific asset classes? Absolutely. Scenarios can be tailored for equities, FX, futures, or crypto markets, each with appropriate microstructure.

What roles does this simulation prepare participants for? It prepares participants for roles such as Quantitative Researcher, Algorithmic Trader, Data Scientist (Finance), and Risk Analyst.

Risk-adjusted returns (Sharpe/Sortino ratios), maximum drawdown, consistency.

Quality of signal research, backtesting discipline, and avoidance of overfitting.

Adherence to risk limits, leverage usage, and response to drawdowns.

Quality of trade execution and minimization of slippage/impact.

Clarity in presenting strategy rationale and performance attribution.

Additionally, peer reviews and final investment committee presentations can be integrated for a comprehensive evaluation.

Join this 20-minute webinar, followed by a Q&A session, to immerse yourself in the simulation.

or

Book a 15-minute Zoom demo with one of our experts to explore how the simulation can benefit you.