Intense, real-world, memorable - gamified simulation training

Intense, real-world, memorable - gamified simulation training

In this FX Options Simulation, participants become currency derivatives traders: managing portfolios, and responding to volatility while balancing risk, reward, and real-time market dynamics in the global foreign exchange marketplace.

FX options pricing fundamentals

Building strategies: Calls/Puts, Straddles, Strangles, Risk Reversals, Butterfly Spreads

Volatility trading: Implied vs. Historical Volatility, Volatility Smiles/Skews

Correlation risk management across currency pairs

Hedging corporate FX exposure using options

Portfolio margin and leverage considerations for options

The impact of interest rate differentials on option valuation

Exotic options concepts introduction

In the simulation, participants will:

Analyze live market data and economic calendars to form a view.

Structure and execute options strategies to express market views or hedge risks.

Actively manage a portfolio, monitoring and adjusting for the "Greeks."

Respond to simulated market shocks and volatility events.

Decide when to cut losses, take profits, or roll positions.

Justify their trading decisions and risk posture in a daily "floor manager" debrief.

Understand the structure, utility, and risks of common FX options strategies.

Apply options pricing theory and the "Greeks" to real-time portfolio management.

Construct options-based solutions for hedging and speculative objectives.

Manage a portfolio's risk exposure under conditions of market stress.

Interpret volatility data and its critical role in options trading.

Build confidence in financial decision-making under uncertainty.

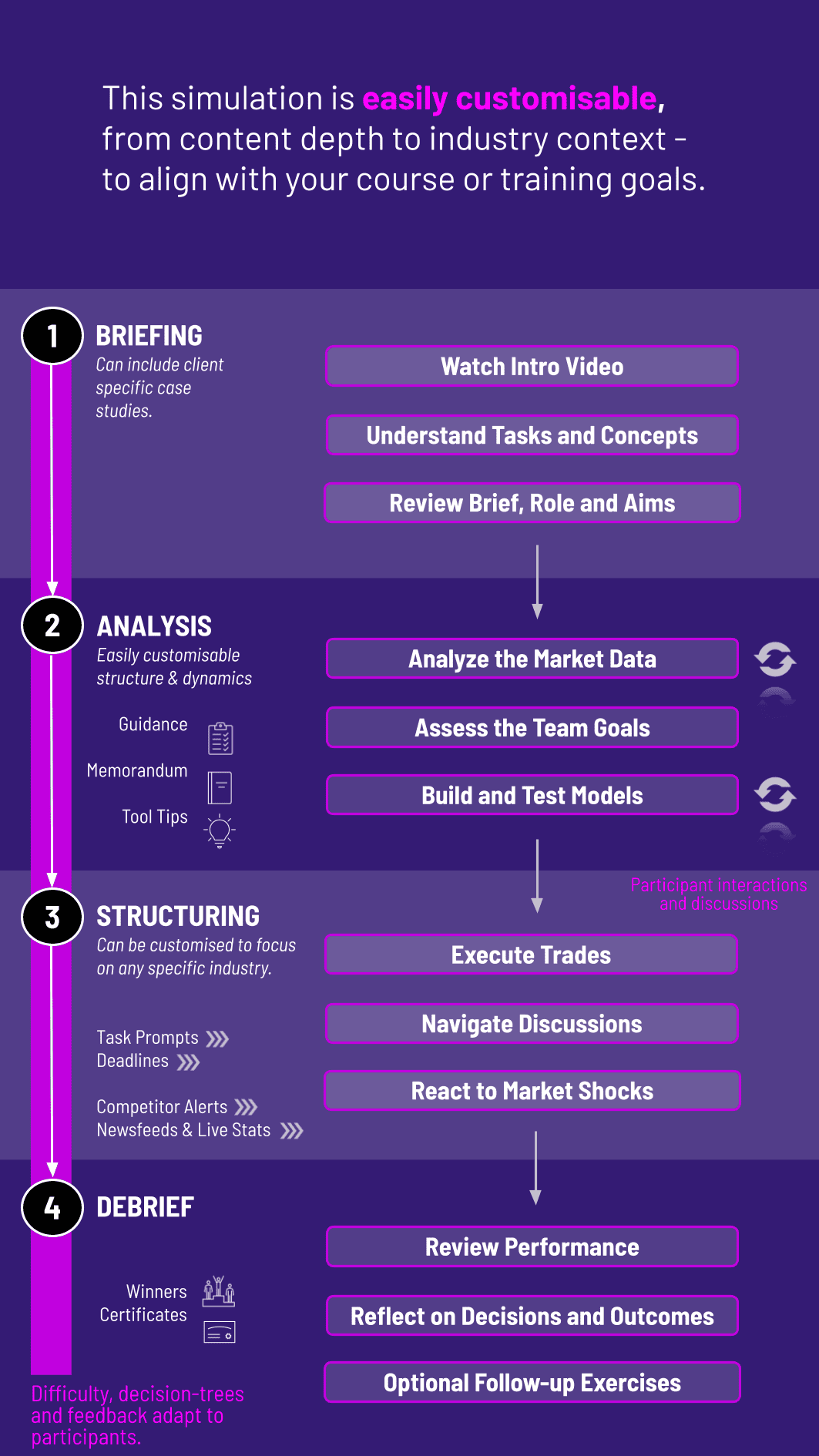

1. Receive Market Brief Participants get a macroeconomic snapshot, client hedging needs, and risk limits.

** 2. Analyze and Plan** Teams analyze spot FX movements, volatility surfaces, and interest rate curves to identify opportunities.

3. Execute and Manage They trade options, build a portfolio, and continuously monitor and adjust their positions.

4. Collaborate Teams debate market views, allocate risk capital, and prepare for the client review.

5. Communicate Outcomes Participants deliver a concise trade rationale and performance summary.

6. Review and Reflect The system provides feedback on P&L, risk-adjusted returns, and Greek exposures. Strategies evolve across multiple rounds

Who is the FX options simulation designed for? It's ideal for MBA students, finance graduates, aspiring traders, and corporate treasury professionals seeking practical, hands-on experience in currency derivatives and risk management.

Do I need prior options trading experience? No prior trading experience is required. The simulation includes foundational instructional content, guided tutorials, and progressive complexity to cater to all levels, from beginners to those with some theoretical knowledge.

How long does the FX options simulation run? The core simulation is designed for 4-6 hours of engaged activity. It can be condensed into an intensive workshop or extended with deeper preparatory theory and analysis modules to suit academic schedules.

Is the simulation individual or team-based? It supports both formats. The team-based format is highly recommended as it replicates the collaborative and high-pressure dynamics of a real trading desk, fostering debate and strategic alignment.

What currency pairs and products are covered? Participants trade major currency pairs and work with vanilla options. The principles learned are directly applicable to a broad range of FX derivatives.

Is the market data realistic? Yes. Participants work with simulated market data calibrated to reflect realistic price movements, volatility patterns, and correlation structures based on historical and plausible scenarios.

Can the simulation focus be customized for our course? Absolutely. Instructors can tailor parameters such as market volatility regimes, specific learning objectives, and the complexity of strategies enabled.

How is trader performance measured? Performance is evaluated on a combination of absolute P&L, risk-adjusted returns, consistency in applying a strategy, adherence to risk limits, and the clarity of trade rationale communicated.

Absolute return, risk-adjusted return, and maximum drawdown.

Effectiveness and consistency in managing Greek exposures (especially Delta and Vega) within stated limits.

Appropriate use of options strategies for stated market views or hedging objectives.

Clarity, logic, and market analysis behind trading decisions during debriefs.

Ability to adjust strategies effectively in response to simulated market shocks.

Join this 20-minute webinar, followed by a Q&A session, to immerse yourself in the simulation.

or

Book a 15-minute Zoom demo with one of our experts to explore how the simulation can benefit you.