Intense, real-world, memorable - gamified simulation training

Intense, real-world, memorable - gamified simulation training

In this Asset Allocation Simulation, participants step into the role of institutional portfolio managers, tasked with constructing and managing diversified investment portfolios across multiple asset classes.

Modern Portfolio Theory and the Efficient Frontier

Strategic vs. Tactical Asset Allocation

Risk-Return Trade-off and Diversification Benefits

Asset Class Characteristics

Correlation Analysis and Portfolio Optimization

Economic Cycle Analysis and Market Regime Detection

Risk Metrics: Standard Deviation, Value at Risk, Sharpe Ratio

Liability-Driven Investment Strategies

ESG Integration in Portfolio Construction

Performance Attribution and Benchmarking

Client Profiling and Investment Policy Statement Adherence

In the simulation, participants will:

Analyze client investment mandates, risk tolerance, and return objectives.

Interpret macroeconomic forecasts and capital market assumptions.

Construct an initial strategic asset allocation across global markets.

Rebalance portfolios in response to simulated market movements and economic shocks.

Decide when to make tactical shifts to capitalize on short-term opportunities.

Present performance reviews and strategic rationale to a simulated investment committee.

Reflect on the outcomes of their allocation choices and adjust their strategy.

Apply the core principles of Modern Portfolio Theory to build diversified portfolios.

Distinguish between strategic, long-term allocation and tactical, short-term adjustments.

Quantify and manage portfolio risk using key financial metrics.

Respond strategically to changing economic indicators and market volatility.

Align portfolio construction with specific client goals and investment constraints.

Communicate allocation decisions and performance clearly to stakeholders.

Evaluate the impact of alternative investments and ESG factors on portfolio outcomes.

Develop confident, evidence-based decision-making under uncertainty.

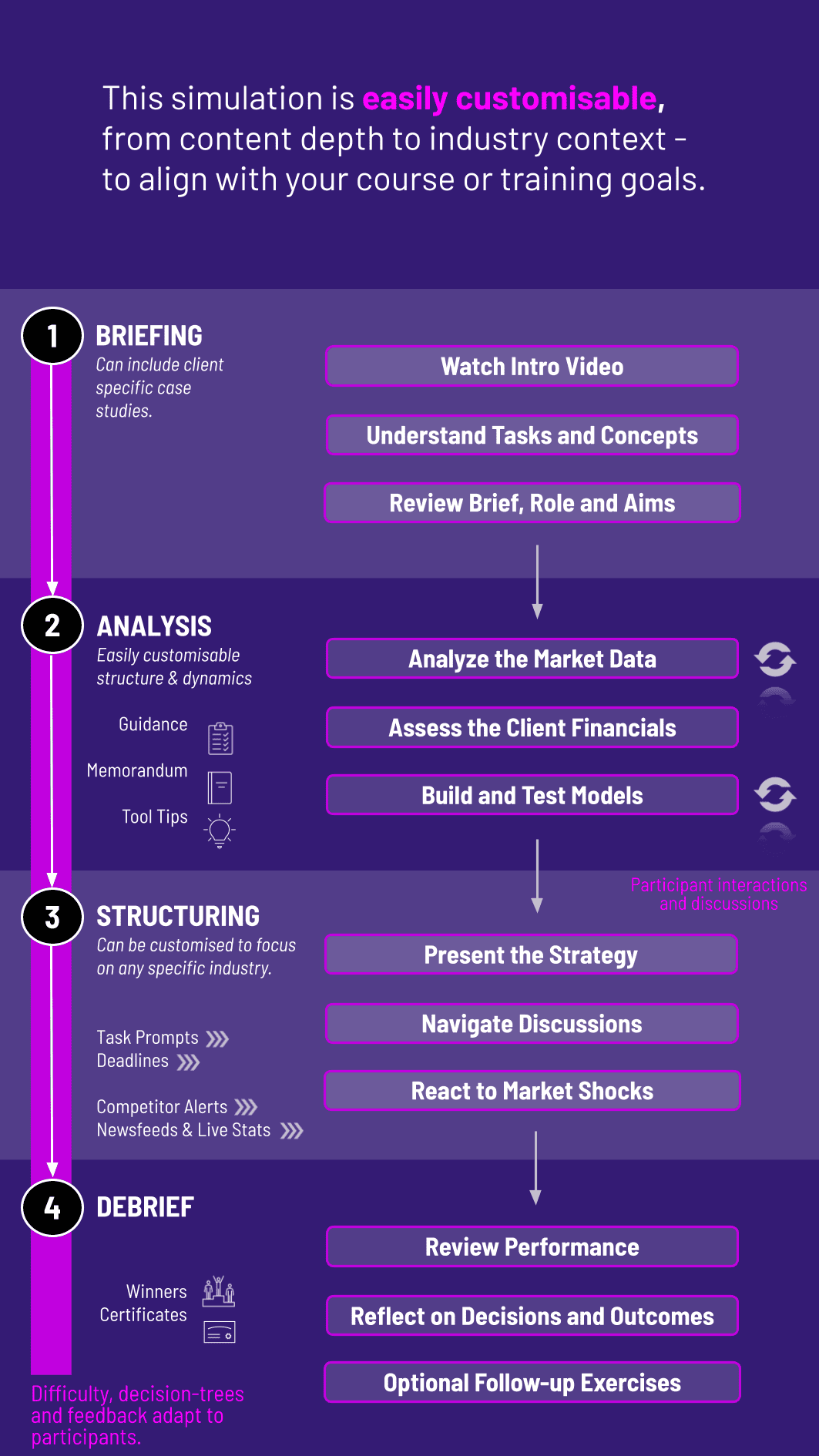

1. Receive the Mandate Teams are assigned a client with a specific Investment Policy Statement outlining goals, constraints, and risk limits.

** 2. Market Analysis** Participants review a dashboard of economic data, asset class forecasts, and current market valuations.

3. Strategic Decision Teams establish their benchmark strategic allocation across major asset classes.

4. Execution and Rebalancing As each round progresses, new market data and events are introduced. Teams must decide whether to rebalance to their target or make tactical over/underweight decisions.

5. Collaboration and Negotiation Teams debate their views, often taking on roles like Chief Investment Officer, Risk Manager, or Equity Strategist.

6. Reporting Participants compile their performance, explain their decisions, and justify their strategy in a concise report or presentation.

7. Review and Iterate Detailed feedback is provided on portfolio returns, risk metrics, and IPS compliance, informing strategy for the next round.

Who is the target audience for this simulation? This simulation is ideal for undergraduate and graduate finance students, MBA candidates, and professionals in fields like asset management, wealth management, and pension fund administration who seek to master portfolio construction.

What prior knowledge do participants need? A basic understanding of financial markets and asset classes is helpful, but not required. The simulation includes introductory content and guides to support all learning levels.

How long does a typical simulation run take? The core experience is designed for 4-6 hours, but it can be condensed into an intensive 3-hour session or extended into a multi-week module with deeper analysis.

Is this an individual or team-based exercise? It is primarily designed for teams to foster debate and collaborative decision-making, mirroring real investment committees, but can be configured for individual participation.

Does the simulation use real market data? Yes, the economic scenarios and asset class return simulations are grounded in realistic historical and forward-looking financial data to ensure authenticity.

Can the simulation focus on specific topics like ESG or alternatives? Absolutely. Instructors can customize parameters to emphasize sustainable investing, increase exposure to private assets, or focus on liability-driven investing for pension funds.

How is participant performance measured? Performance is multi-faceted, evaluated on risk-adjusted returns (e.g., Sharpe ratio), adherence to the client's investment mandate, the quality of strategic reasoning, and the clarity of communication.

What career skills does this simulation develop? It builds practical skills for roles such as Portfolio Manager, Investment Analyst, Wealth Advisor, and Risk Officer, with a strong emphasis on analytical decision-making and client communication.

Risk-adjusted returns relative to a benchmark and peer groups.

Effectiveness in controlling volatility and drawdowns during market stress.

Success in staying within the client's IPS constraints and strategic goals.

Quality of analysis and justification for allocation decisions.

Clarity and persuasiveness in reporting to the investment committee.

Join this 20-minute webinar, followed by a Q&A session, to immerse yourself in the simulation.

or

Book a 15-minute Zoom demo with one of our experts to explore how the simulation can benefit you.